Antimony 18 Months On: Did the Squeeze Break, or Is This the New Floor?

Antimony 18 months after the squeeze: where prices settled, why the China-versus-rest price gap persists, and how buyers should contract for 2026–2027.

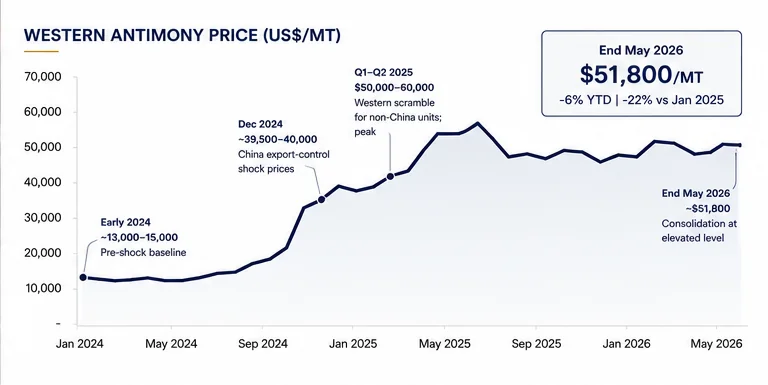

Antimony traded near $51,800 per metric ton at the end of May 2026. Eighteen months ago we wrote that prices had risen 27-fold; the question now is not whether the spike was real, but where the market settles.

When we last covered antimony in November 2024, the metal had gone parabolic. Western spot prices climbed through $39,500 per ton by the end of 2024 and pushed to $50,000–$60,000 across the first half of 2025. That move was driven by one fact: China, which controls the majority of mined and refined supply, had moved antimony onto its export-control list. Buyers outside China scrambled, and the price did the rest.

A year and a half later the picture is calmer but not cheap. Prices have come off the 2025 highs, yet they sit far above anything seen before 2024. For buyers the practical question has changed. It is no longer how high this goes, but whether this elevated level is the new normal, and how to contract around it. Our read is that it largely is.

Where the price actually is

Antimony ended May 2026 around $51,800 per ton, down roughly 6% year-to-date and around 22% below where it sat at the start of 2025. In other words, the peak is behind us, but the floor has reset to a level that would have looked absurd two years ago. The metal has not given back its gains; it has consolidated.

Period | Western price ($/MT) | Driver |

Early 2024 | ~$13,000–15,000 | Pre-shock baseline |

Dec 2024 | ~$39,500–40,000 | China export-control shock prices in |

Q1–Q2 2025 | $50,000–60,000 | Western scramble for non-China units; peak |

End May 2026 | ~$51,800 | Consolidation at elevated level |

The two-price market is still here

The defining feature of this cycle is not the headline number, it is the split. Export controls opened a gap between what antimony costs inside China and what it costs everywhere else. Through 2025 Chinese domestic offers were reported as low as roughly $14,000 per ton while Western buyers paid $55,000–60,000 — close to a four-fold difference for the same metal.

That wedge is the single most important thing for a buyer to understand. It is not a pricing error; it is policy. Material is cheap where it cannot freely leave and expensive where it is needed. Most market participants expect the gap to narrow over the coming year as trade flows normalise and more raw material moves back into China, but narrowing is not closing. As long as the licence regime exists, origin and paperwork carry a premium.

China dialled back, but did not let go

There has been a genuine policy thaw. In November 2025 China’s Ministry of Commerce suspended its export ban on antimony — along with gallium and germanium — for shipments to the United States, with the suspension running to late November 2026. That took some heat out of the panic.

The word that matters is suspended. A suspension with an expiry date is not a repeal. It is a window that can close again, and any buyer building a 2027 supply plan around Chinese material is building on a permission that has a clock on it. The smart reading is to treat current access as a convenience, not a foundation.

Why demand is not going to rescue buyers

Roughly half of antimony demand is still flame retardants, the traditional anchor. The change underneath is what the other half is becoming.

Solar glass. Antimony trioxide is a clarifying agent in solar cover glass. Consumption from the solar sector is forecast to reach around 68,000 tons in 2026, up from roughly 16,000 tons in 2021 — taking photovoltaics from about 11% of antimony demand toward 39%.

Defence. Antimony hardens lead for ammunition and is used in armour-piercing rounds, primers, and night-vision optics. The US Department of Defense alone specifies it across more than 200 types of ammunition.

This is the uncomfortable part for procurement. The two fastest-growing demand sources — the energy transition and national security — are both highly price-inelastic. A solar manufacturer or a defence prime does not stop buying because antimony is expensive; the metal is a tiny share of their finished cost and there is no substitute. They bid against each other for a metal that has been in structural deficit since 2022, while Chinese mined supply in 2025 ran roughly 24% below 2021 levels as its richest deposits deplete.

Where the alternative tons come from

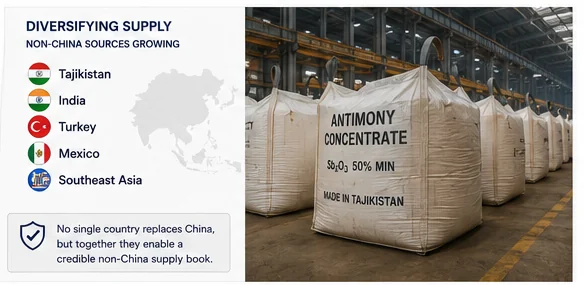

The one piece of genuinely good news is that non-China supply is responding. Southeast Asian growth is expected to keep the global balance adequate in 2026, and buyers diversifying away from China have pulled more processed metal from Tajikistan, India, Turkey, Mexico, and across Southeast Asia. None of these individually replaces China, but together they give a buyer something to build a non-China book around — which two years ago barely existed.

Au Club’s read for the next 12 months

- The spike is over; the re-rating is not. We do not expect antimony to return to pre-2024 levels. A $45,000–55,000 working range is the realistic base for 2026, with the floor reset structurally higher.

- The two-price market persists. The China-versus-rest gap narrows but stays open while licences exist. Non-China origin keeps a premium worth paying for buyers who need supply security.

- Treat Chinese access as borrowed time. The export-ban suspension expires in late 2026. Build 2027 plans on diversified, non-China origin and treat any Chinese flow as upside, not the base.

How Au Club helps

Au Club supplies antimony ingots and antimony concentrate with independently inspected, documented origin. For buyers serving solar, defence-adjacent, or other security-sensitive end markets, we can confirm non-Chinese origin and structure spot or term supply, FOB UAE, with SGS or equivalent inspection on every cargo. LC and TT accepted. Talk to the desk about locking 2026 volume and opening 2027 forward arrangements before the policy window changes again.

FAQs

Is antimony going to keep falling?

It has come off the 2025 peak, but our base case is consolidation in the $45,000–55,000 range rather than a return to old lows. The deficit and demand drivers remain intact.

Why is Chinese antimony so much cheaper?

Export controls trap cheaper material inside China while buyers outside pay a security premium. The gap is policy-driven, not quality-driven.

Can I still buy Chinese antimony?

For now, yes — the export-ban suspension runs to late November 2026. After that, access depends on policy. Plan for non-China origin as your base.

Where does Au Club source non-China antimony?

Across Southeast Asia and producers in Tajikistan, India, Turkey, and Mexico, with inspected origin documentation.

About Au Club

Au Club is a Dubai-based commodity trading company supplying marine fuel, metals, and minerals worldwide. We trade antimony concentrate and antimony ingots from non-Chinese origins, with SGS or equivalent pre-shipment inspection and full documentation. To enquire about availability and pricing, contact our trading desk.