Tin’s Demand Story Nobody Prices In: Solder, Semiconductors and the AI Build-out

Tin's demand story for 2026: how solder, semiconductors and the AI data-centre build-out are driving a structural deficit, and what it means for tin buyers.

Tin pushed toward $50,000 per ton in 2026, up around 70% on the year. The supply squeeze gets the headlines. The quieter story is on the demand side — and it runs straight through the AI build-out.

Last autumn we wrote about tin supply, and why Thailand had become a more reliable source than Indonesia. That piece was about where the metal comes from. This one is about why it is suddenly so wanted. Because the part of the tin story that markets keep underpricing is not the mines — it is the solder.

Around half of all tin consumed goes into solder, and solder is what holds electronics together. Every server, every chip on a board, every power module and networking switch in a data centre is joined with tin-based solder. When the hyperscalers commit to spending, tin demand is downstream of that decision whether anyone names the metal or not.

The numbers behind the move

Metric | 2026 reading |

Tin price | ~$50,000/MT, up ~70% year-on-year |

H1 2026 average | ~$45,000/MT (+40% YoY) |

Solder share of demand | ~50% of global tin consumption |

Refined supply growth 2026 | ~+3% |

Demand growth 2026 | ~+3.5% — market tips into deficit |

First deficit since | 2021 |

Supply from unstable regions | ~60% of global production |

Why AI is a tin story

The link is indirect, which is exactly why it is underpriced. AI does not consume tin directly. AI consumes servers, and servers consume solder. Major cloud providers have announced data-centre capital expenditure running past $100 billion a year through 2026. That spending lands as racks of hardware, and every board in those racks is soldered.

Crucially, data-centre build-out is additive demand. It sits on top of the ordinary replacement cycle for phones, cars, and consumer electronics rather than replacing it. So at the very moment supply is struggling, a large new layer of demand has been switched on — one tied to multi-year capex commitments, not a seasonal upgrade. That is what turns a tight market into a deficit.

And supply cannot answer quickly

Refined production is expected to grow about 3% in 2026, short of roughly 3.5% demand growth. The result is the first deficit since 2021. The reason supply cannot simply ramp is geography: around 60% of global tin output comes from politically unstable jurisdictions, and the two swing sources are both impaired.

Myanmar. The Wa State mining ban imposed in August 2023 took out a huge slice of feed to Chinese smelters. The core Man Maw area — roughly 80% of Myanmar’s supply — has been largely suspended, and Myanmar’s share of China’s imports fell to around 24–30% in 2025. The International Tin Association reports shipments are set to resume as operators secure new three-year permits, but a restart is not the same as full output.

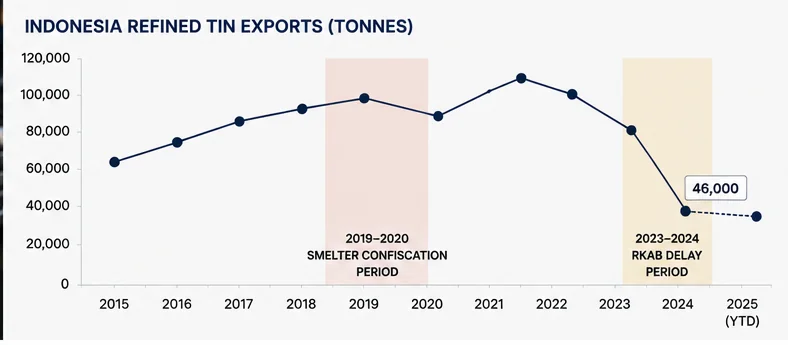

Indonesia. Exports keep being throttled by delays in approving annual work permits, making the world’s largest exporter an unreliable swing producer.

DRC. The Democratic Republic of Congo became China’s largest tin concentrate supplier in early 2025, with its import share rising to around 28%. Supply growth there is real but constrained, and security risk is ever-present.

The Gulf angle worth noting

There is a Gulf thread in the tin supply story that is easy to miss. Abu Dhabi’s sovereign wealth interests took majority ownership of Alphamin, the operator of the Bisie mine in the DRC and one of the most significant non-Asian tin producers. Combined with US-brokered security arrangements in the region, that signals rising institutional confidence in a jurisdiction that now sits near the centre of global tin supply — and it puts Gulf capital directly into the metal’s future.

What this means for buyers

For anyone consuming tin or tin concentrate, the demand-side story changes how you should think about price risk. This is not a spike waiting to mean-revert; it is a structural deficit met by impaired supply, with a new and committed buyer in the data-centre sector. The downside case requires either an AI capex pause or a clean supply restart in Myanmar and Indonesia at the same time — possible, but not the base case.

- Assume the floor is higher. Solder demand is sticky and growing. Budget for tin holding well above the old comfort range.

- Diversify origin. With 60% of supply in unstable regions, concentration is the real risk. Spread across producers and document origin.

- Contract on a benchmark, not a fixed price. Volatility is too high for long fixed-price deals; use an LME-referenced formula with origin and volume flexibility built in.

How Au Club helps

Au Club trades tin concentrate with inspected, documented origin and the flexibility to source across multiple producing regions rather than a single point of failure. We structure spot and term supply, FOB UAE, with SGS or equivalent inspection on every cargo, LC and TT accepted. For buyers exposed to the electronics and data-centre demand wave, the desk can help build an origin-diversified book and contract structure that survives a volatile market.

FAQs

Why is tin rising so fast?

A structural supply deficit meets new, additive demand from data-centre and AI hardware build-out — all of which is assembled with tin solder.

How much tin does electronics really use?

Solder is roughly half of all tin demand, and it is the dominant use in semiconductors and electronics assembly.

Will Myanmar supply coming back end the deficit?

A restart helps, but a phased resumption under new permits is unlikely to fully close a deficit that demand growth keeps widening in 2026.

Where does Au Club source tin concentrate?

Across multiple producing regions, with inspected origin documentation and origin flexibility for buyers who need it.

About Au Club

Au Club is a Dubai-based commodity trading company supplying marine fuel, metals, and minerals worldwide. We trade tin concentrate with SGS or equivalent pre-shipment inspection and full origin documentation, FOB UAE. To enquire about availability and pricing, contact our trading desk.